As we move through the first quarter of 2026, the global financial landscape is undergoing its most significant transformation since the early 2000s. The “War of 2026″—a term now synonymous with the overlapping regional conflicts and the breakdown of traditional trade routes—has fundamentally altered how sovereign credit ratings are calculated.

At Al Taiff, we recognize that in this era of “Polycrisis,” a country’s creditworthiness is no longer just about its balance sheet. It is about its resilience, energy security, and geopolitical alignment.

The Evolution of Credit Risk: Beyond the Balance Sheet

Historically, agencies like S&P Global, Moody’s, and Fitch focused heavily on a nation’s Debt-to-GDP ratio and fiscal deficit. In 2026, these metrics have been joined by a new, more volatile set of indicators:

- Supply Chain Sovereignty: In a world of disrupted shipping lanes, countries that control their own natural resources—specifically aluminum, copper, and energy—are seeing their credit outlooks stabilize.

- Defense Burden-Sharing: For the first time in decades, massive increases in defense spending are being viewed as a “fiscal drag.” Nations that must borrow heavily to modernize their militaries are facing downward pressure on their investment-grade status.

- Cyber-Resilience: As hybrid warfare becomes the norm, a nation’s ability to protect its financial infrastructure from state-sponsored cyberattacks is now a qualitative factor in its credit rating.

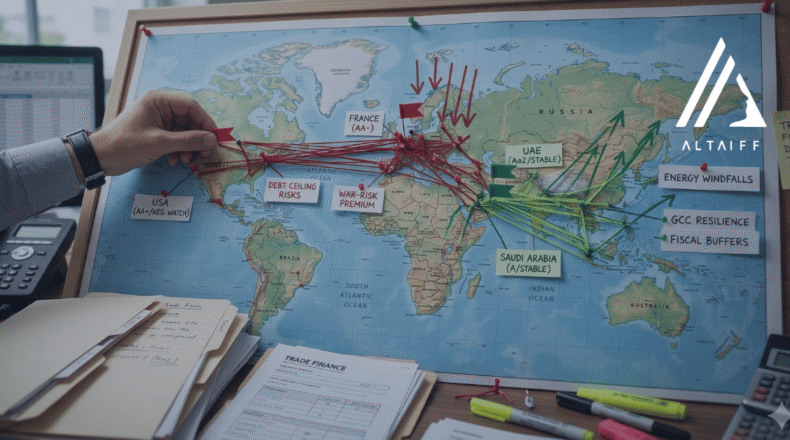

Regional Deep-Dive: Winners and Losers of 2026

The credit map of 2026 is one of sharp contrasts. While some regions have found stability through high commodity prices, others are struggling under the weight of inflationary debt.

1. The GCC: The Global Anchor

The United Arab Emirates (Aa2/AA) and Saudi Arabia have emerged as the “Safe Harbors” of 2026.

- The UAE Advantage: With its diversified economy and massive Sovereign Wealth Funds (SWFs), the UAE maintains a “Stable” outlook. Its role as a global logistics and financial hub has only strengthened as other traditional markets face volatility.

- Energy Windfalls: High global energy prices have allowed these nations to self-fund ambitious infrastructure projects without increasing their external debt, a rarity in the current global climate.

2. Europe: The Fiscal Squeeze

Across the Eurozone, the “War of 2026” has forced a difficult choice between social spending and regional security.

- France (AA-): France remains under a “Negative Watch.” The combination of high public debt and the necessity of funding a pan-European defense response has raised concerns about long-term fiscal sustainability.

- Germany (AAA): While still the gold standard for European credit, Germany’s industrial sector is grappling with high energy costs, leading to a “cautious” sentiment among investors regarding its future growth prospects.

3. The United States: The AAA Question

The most debated credit story of 2026 is the United States (AA+ / Negative Outlook).

- Debt Ceiling Brinkmanship: Recurrent political gridlock over the national debt, which has surged past $36 trillion, continues to haunt the markets.

- The Dollar’s Dominance: Despite fiscal concerns, the US dollar remains the world’s reserve currency. This “exorbitant privilege” prevents a total credit collapse, but the risk premium on US Treasuries has hit a 20-year high.

2026 Sovereign Credit Index

| Country / Region | 2026 Rating Trend | Primary Risk Factor | Strategic Opportunity |

| UAE & Qatar | Stable / Upward | Regional Spillovers | Diversification into AI & Tech. |

| India & SE Asia | Positive | Energy Import Costs | “Friend-shoring” Manufacturing. |

| United States | Negative Watch | Fiscal Deficit & Polarization | Unmatched Liquidity & Innovation. |

| Egypt & Turkey | Vulnerable | Currency Volatility | Strategic Geographic Positioning. |

| West Africa | Under Pressure | High Interest Rates | Mineral Wealth (Lithium/Cobalt). |

How These Ratings Impact the Private Sector

For businesses and individual investors, a change in a country’s sovereign rating is the first domino in a series of financial impacts:

- The Sovereign Ceiling: Most companies cannot have a credit rating higher than their home country. A national downgrade automatically makes corporate borrowing more expensive for local businesses.

- Trade Finance Bottlenecks: In 2026, international banks are increasingly hesitant to confirm Letters of Credit (LCs) from “High-Risk” jurisdictions. This directly impacts the trade of vital commodities like aluminum ingots and copper cathodes.

- Capital Flight: When a rating drops, institutional investors often pull their “hot money” out of the country, leading to sudden currency devaluation and increased cost of living for the population.

Navigating the Future with Al Taiff

The current global climate reminds us that the economy is an extension of geography and security. Whether you are managing private wealth or overseeing international trade, the credit health of the nations you operate in is your most important metric.

In 2026, staying ahead means looking beyond the headlines. It means understanding the deep-seated fiscal trends that will define the next decade of global finance.